By Anton Tagliaferro

WATCH

READ

As we move into 2022, the mainstream news continues to be dominated by Covid while financial markets remain wary of central bank policy given that the Fed has signalled higher US rates in 2022 as inflation and economic growth continue to pick up.

So where should investors now be focused?

We are now two years into the outbreak of Covid and while the mainstream media headlines continue to be dominated by the record number of new Omicron cases, it appears that we’re entering the later stages of the pandemic. While Covid case numbers are reaching highs of 100,000 per day in Australia, it appears that the new variant is a less harmful virus as the number of patients entering ICU every day has remained very low.

Omicron is effectively ‘burning out’ the Delta variant around the world, with some countries claiming the Delta variant has all but vanished. We are also encouraged to see the declining Omicron daily case numbers in countries like South Africa, where the variant originated in November last year.

What this means, is that while we may still see further stress on the healthcare system and supply chains with increasing numbers of workers entering isolation, we believe it is highly unlikely that we will see the severe lockdowns and travel bans that we have experienced in the last two years.

Why is this relevant to investors you may ask?

This news is very relevant as it means that central banks can now look forward to a future where the economy will continue on its current path, allowing them to normalise the ultra-easy monetary policy that has been in place since March 2020. At that time, lockdowns and travel bans forced the hand of central banks into easing aggressively by cutting interest rates to zero and announcing huge bond buying programs to lower bond yields to ensure that the world avoided a large-scale economic downturn.

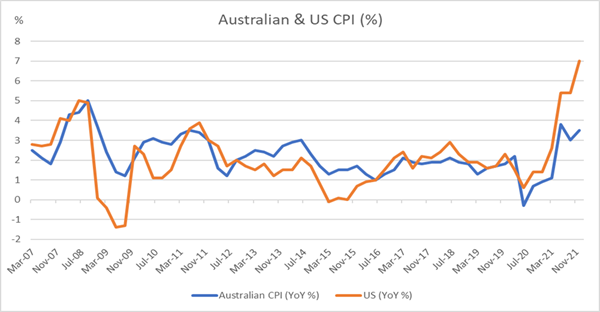

While central bank policy has succeeded in helping world growth recover strongly from the economic downturn caused in 2020 and 2021, we have also recently seen inflation spike in many countries due to a combination of higher energy costs, supply shortages in various key manufacturing industries and soaring shipping costs.

Source: Bloomberg; March 2007 – December 2021

In the US, the Federal Reserve has signalled its intent to raise interest rates in March following a rapid rise in inflation to 7 percent in December. In Australia, inflation is also running at levels not seen in more than 20 years, prompting interest rate markets to price in hikes earlier than the Reserve Bank has forecast.

Clearly if central banks decide that inflation is becoming entrenched then they will not be able to maintain their zero interest rate policies for much longer and will have to move more aggressively than expected in terms of normalising interest rates in the years ahead.

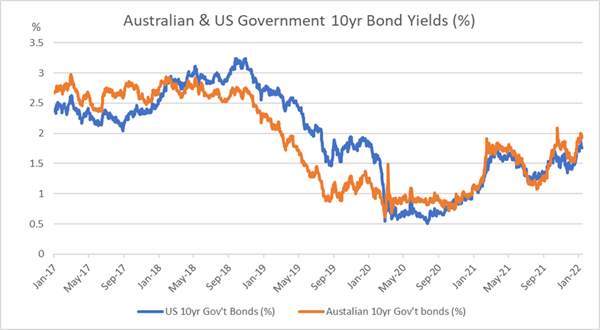

Whatever the case – and we are not economic forecasters – whether inflation settles at 2, 3, or 4 percent, or higher, it is clear that the era of zero interest rates in response to the pandemic in many parts of the world, such as the US the UK and Australia, is coming to an end. In addition, it also means the end to the aggressive buying of bonds by central banks – a move which has artificially lowered bond yields significantly in many parts of the world since 2020. This means that bond yields will also move higher than where they have been trading in the last two years.

Source: Bloomberg; January 2017-January 2022

So, what does this mean for equities and where should one’s portfolios be positioned?

In a world of zero interest rates, you can pay almost any price for future growth because of the risk-free rate, as represented by government bond yields. It should therefore not be surprising that growth stocks have performed so strongly in the last few years.

However, the return of inflation means that the Fed and other central banks around the world will be forced to increase interest rates, which means that what you want as an investor is current cash flow, not 2040 or 2050’s cash flow discounted back.

Inflation is about to resolve that issue. Replacement costs are rising, and financing costs will increase going forward. Return thresholds will suddenly have bond rates of more than zero to compete with.

Stocks like Aurizon (ASX:AZJ), Orica (ASX:ORI) and Pact Group Holdings (ASX:PGH) have underperformed significantly in recent years because of short-term, Covid-related issues and have been shunned by many investors who instead preferred to chase growth stocks. With interest rates rising these stocks suddenly don’t look so boring or dull as things normalise and as investors begin to appreciate real cash flows generated by companies in the next two-to-three years, as opposed to hoped-for cash flows in 10 or 20-years’ time.

We have included more detail on these stocks below.

We believe highly priced growth stocks, or speculative stocks, will likely see a material de-rating as interest rates and hence the discount rates rise. At the current point in this cycle even small increases in interest rates can have a large negative impact on share prices, as valuation multiples for many growth stocks are so high that a 100 basis points of interest rate rises today is far more material compared to any other time in current investors’ memories.

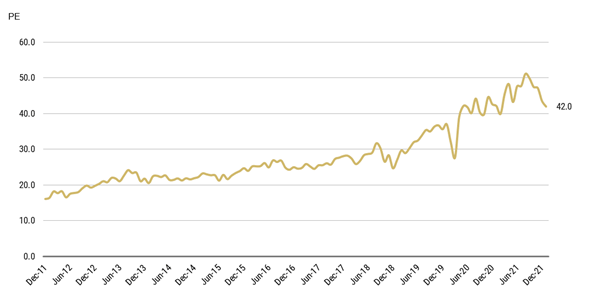

The chart below illustrates the growth in earnings multiples for the top quartile of ASX 200 companies, trading at a significant premium to the historical average.

Top quartile price to earnings ratios of the ASX200

Source: Morgan Stanley

IML’s portfolios are thus positioned in companies whose valuations make sense in a higher interest rate world. We continue to focus on real companies which have a durable competitive advantage, and that typically have substantial real assets or long-term, monopoly-like licenses (not start-ups). All of the companies in IML’s portfolios produce strong and recurring cashflows today and they are run by experienced and well credentialled management teams. We believe that all of the companies in our portfolios have very positive outlooks over the next three-to-five years.

Conclusion

The last few years have been good ones for equity investors – especially growth focused ones – as most central banks around the world cut rates to zero and embarked on extremely stimulative policies. Going forward, as we see these policies reverse, we believe the environment will require equity investors to be far more selective.

One of the biggest challenges both investors and their advisers face today is that there is an unavoidable over reliance on growth assets to create wealth. Now, more than ever, it’s important to make sure growth assets don’t destroy a client’s wealth. With interest rates almost certainly to be on the rise in 2022, the sustainability of the returns from growth and speculative stocks is likely to be severely tested. Despite markets being close to all-time highs, and with many valuations being fairly high, we continue to find opportunities to invest in good quality stocks that we believe have strong competitive advantage, generate good cash flow, are managed by very credible and competent management teams, and where the outlook for the next three-to-five years looks very favourable.

We think this will be a key factor to the prospective return outlook of our funds, where we remain optimistic of doing well going forward, after delivering solid returns across all our funds in 2021.

Anton Tagliaferro is IML’s founder and Investment Director. He is a Portfolio Manager of IML’s Australian Share Fund, All Industrials Share Fund, Equity Income Fund and Private Portfolio Fund.

Additional information on stocks mentioned above

The following shares we hold in our portfolios stand out in a market where many stocks look fully priced.

Aurizon (ASX:AZJ)

Aurizon is the monopoly owner of the Central Queensland Coal Rail Network and an operator of coal trains and wagons in QLD and NSW. The company also has a bulk transport business, moving vital commodities and other freight, to and from customers across mainland Australia.

The largest value driver of the company is its rail network, which is a regulated asset, meaning the company earns very stable, predictable cash flows and profits every year. Its customer base is predominately metallurgical coal customers, which have long-life, low-cost mine assets. Aurizon’s coal transport business together with bulk transport should provide shareholders with predictable profits and dividends, capable of supporting a dividend yield of 7-8 percent per annum, or more than 28 cents per share, for decades to come.

In response to an eventual decline in coal volumes, Aurizon is actively looking to expand the bulk transport part of its business. Its recent purchase of One Rail Australia, slated to settle in the first half of this year, is designed to significantly lift Aurizon’s exposure to non-coal rail transport. As part of the transaction, Aurizon will need to sell One Rail’s coal haulage business (due to competition concerns) but will acquire a bulk intermodal business in SA and the NT that owns monopoly lease rights over 2,460km of rail track, plus locomotives, wagons and other ancillary assets.

We believe the acquisition will provide the company with compelling opportunities to transfer surplus coal locomotives and wagons into other contracts over time and it will provide attractive, low capital intensity growth options for the company.

Orica (ASX:ORI)

The global leader in explosives remains out of favour, despite clear signs of a recovery in mining volumes and explosive prices. Orica has faced a tough couple of years due to Covid disruptions, which have impacted mining output and explosives demand. This led to falling explosive volumes and prices and low plant utilisation which significantly impacted Orica’s margins and profits.

Looking forward though the outlook is positive. Commodity prices have risen substantially and many are at, or close to, record highs. In addition to this, Covid disruptions are now reduced and mining volumes are expected to recover strongly during 2022. Explosive prices have also been rising sharply recently from lows of $500/t to $700/t, which is above pre-Covid levels.

In addition, during the pandemic slowdown Orica has continued to invest in its business, particularly in its technology and software products, which have grown substantially. And while these products only represented a relatively small percentage of Orica’s profits pre-Covid, they could potentially represent more than a quarter of the company’s profit in three years’ time.

Despite all this, the share price is still only 15 percent above its Covid lows. We see substantial upside to the company’s cashflows, dividends and share price over the next 2-3 years.

Pact Group Holdings (ASX:PGH)

Pact is a leading supplier of rigid packaging products for the food and beverage sector in Australasia. It’s also a leading provider of re-use products for the grocery and retail sectors which contribute to reducing waste in the circular economy.

Pact has faced a few mixed years due to poor execution in its core packaging business and recently has been impacted by the temporary impact of higher input costs and freight inflation brought about by Covid disruptions. Looking ahead, the core packaging business has been restructured and the company is now investing heavily in differentiating its offer to customers. This includes the recently completed PET recycling facility in Albury (the first of multiple recycling facilities in Australia), which will accelerate Pact’s use of recycled content in its packaging products and is expected to lead to improved margins and customer retention over time.

The re-use pallet business in grocery (Aldi, Woolworths) and hanger business in retail (US Target) has a strong growth outlook driven by the sustainability goals of its customers who are all aiming to reduce their packaging waste. Despite the improving outlook, the stock is trading on an earnings multiple of around ten times forecast 2023 earnings and we expect strong upside to the share price, earnings and dividends over the next few years.

While the information contained in this article has been prepared with all reasonable care, Investors Mutual Limited (AFSL 229988) accepts no responsibility or liability for any errors, omissions or misstatements however caused. This information is not personal advice. This advice is general in nature and has been prepared without taking account of your objectives, financial situation or needs. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to buy, sell, or hold that stock. Past performance is not a reliable indicator of future performance.

INVESTMENT INSIGHTS & PERFORMANCE UPDATES

Subscribe to receive IML’s regular performance updates, invitations to webinars as well as regular insights from IML’s investment team, featured in the Natixis Investment Managers Expert Collective newsletter.

IML marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected by Natixis Investment Managers Australia, on behalf of IML. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.