By Marc Whittaker

READ

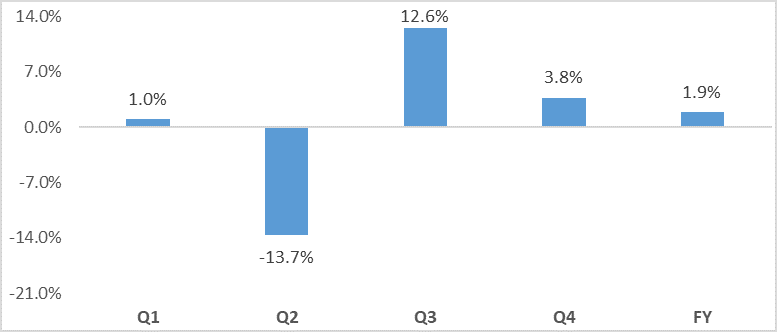

Despite a volatile last 12 months, the Australian small caps sector performance has lagged the overall ASX 300’s returns, and the Small Ordinaries index has remained largely unchanged over the last 12 months – as shown in the graph below.

Small Ords quarterly returns to 30 June 2019

Source: IRESS, IML

The returns from the Small Ords sector have also been characterised by a narrowing base of returns mainly from technology and other ‘high-growth’ stocks where momentum buying appears to have pushed their share prices to levels which, in our view, are well beyond their fundamentals. The buying in many of these sectors has been led by quant-based funds chasing short-term earnings momentum and, as many stocks in these sectors have risen in price, buying from passive/index-linked funds has inevitably followed – leading to very lofty share prices in these cases.

The REITs sector has also been drastically rerated, particularly in the last six months of the financial year as interest rates have declined and many investors have chased anything offering a stable yield. For this reason, most REITs are now trading at substantial premiums to their underlying net tangible asset (NTA) backing – a situation which is unsustainable in our view – with many common-sense investors asking themselves, ‘Why should $1 worth of physical property be valued at $1.50 when listed on the stockmarket in a REIT?’

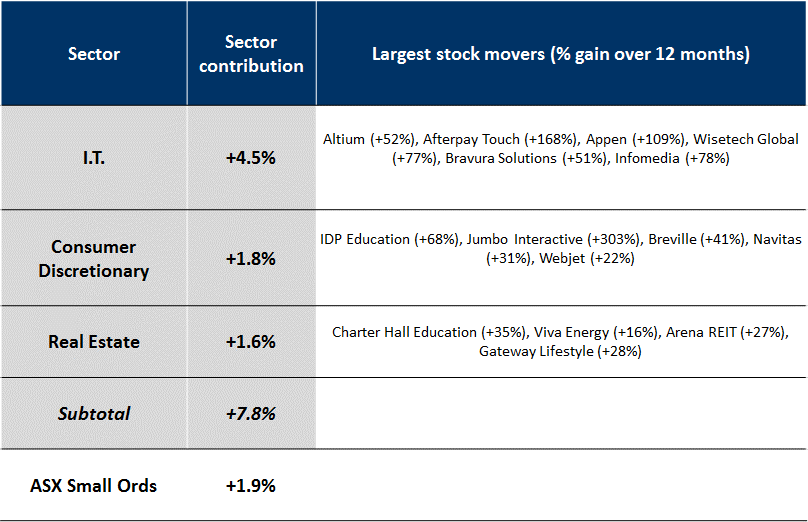

The Small Ords’ returns over FY19 would have been even more lacklustre had it not been for the contribution from three sectors that captured many investors’ attention – namely REITs, Information Technology and Consumer Discretionary, which contains stocks such as international student placement and language testing company IDP Education and digital lotteries retailer Jumbo Interactive. The main sector contributions for FY19 to the Small Ordinaries Index are shown in the table below.

Small Ords’ main sector contributors in FY19

Source: Factset, IML

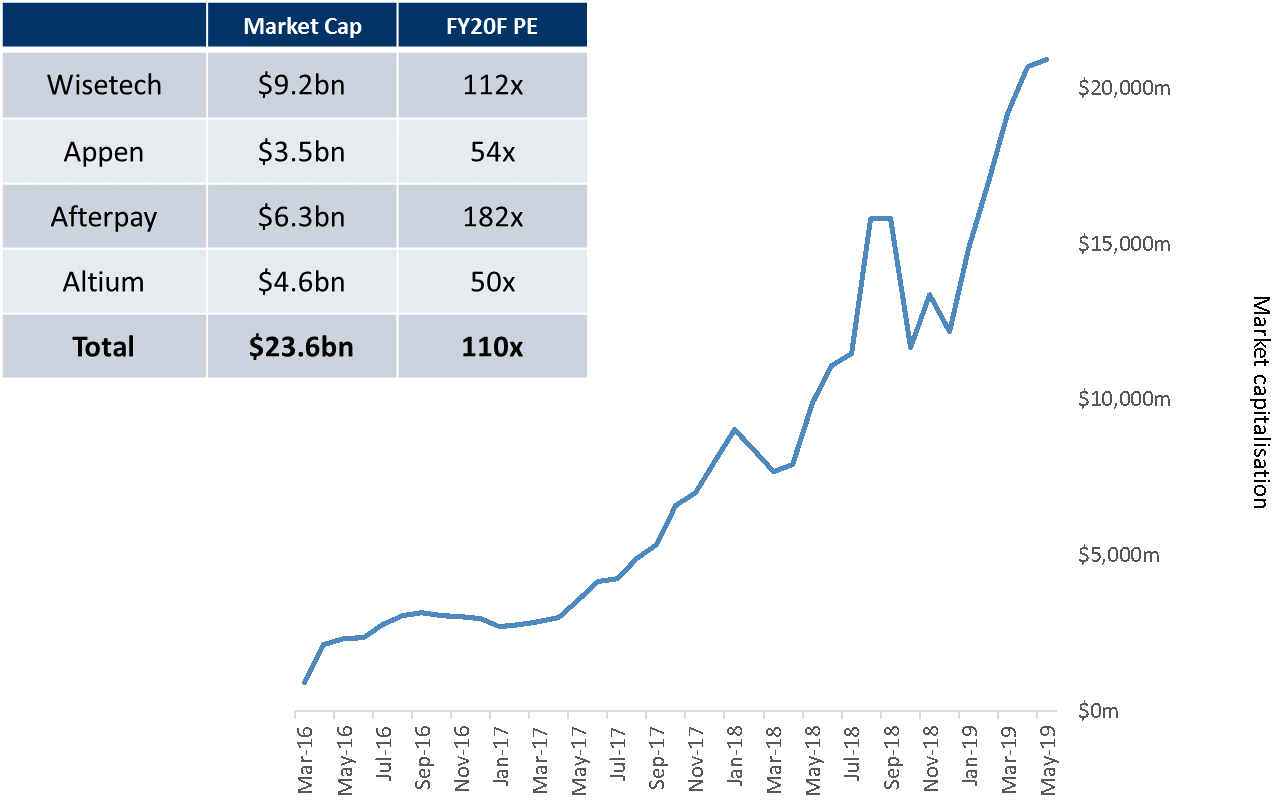

If we look at the IT sector in Australia and focus on the performance of the WAAA* stocks, the IT sector (Wisetech, Appen, Afterpay and Altium) now represents more than 10% of the Small Cap index, thanks largely to the aggregate market cap of these four companies having risen from $1bn in March 2016 to well over $23bn today – a staggering leap in value.

While the earnings of these companies have grown over the last couple of years, the major reason for this jump in the value of their market caps has been a huge rerating of these companies, with their average PE now well over 100x FY20 expected earnings – as seen in the table and chart below.

Source: IRESS, Factset

*The acronym is usually WAAAX because it uses Xero in the grouping. However, Xero is no longer a small-cap stock, having been added to the ASX 100 in 2019.

Have we seen this type of investor behaviour before?

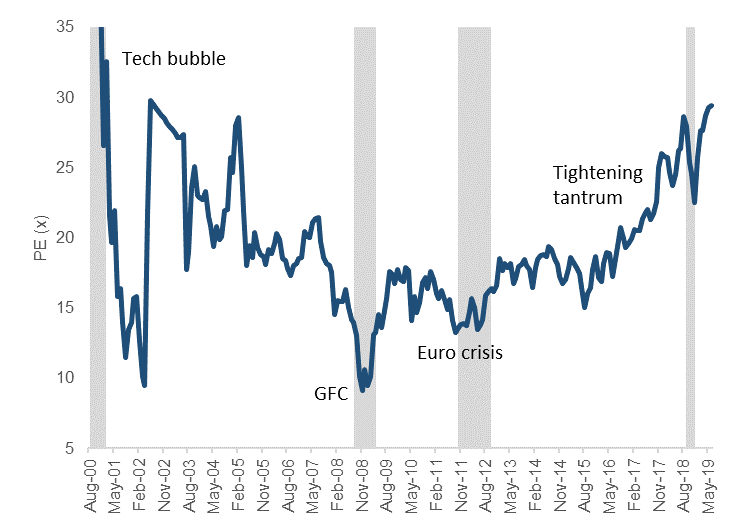

Excessive valuations in stocks or segments of the market which capture investors’ imaginations at various times are nothing new. Any seasoned investor knows that, while in the short-term certain stocks or sectors can overshoot to levels previously unimaginable, over the longer term, markets always tend to return to equilibrium. The PE multiple of the listed IT sector in Australia today mirrors similar peaks seen in the 1999-2000 years when the heroes of that age – such as Solution 6, Sausage Software and Davnet – while all marginally profitable companies at the time – captured many investors’ imaginations and were pushed to elevated levels as these then ‘new economy’ companies were each valued at billions of dollars.

The IT sector’s overall PE, including the WAAA stocks which were used to determine the sector average, is shown in the chart below.

Tech valuations seem to be back in bubble territory

Source: Citi, IML

In our opinion what we are seeing today is not a new valuation paradigm; we seem to be in the middle of another good, old-fashioned bubble.

As Mark Twain is often reputed to have said: “History never repeats itself, but it often rhymes.”

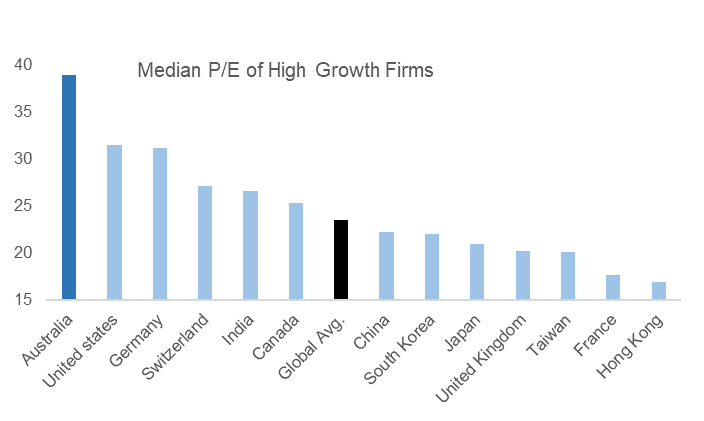

It is also worth noting that ‘high growth’ stocks in Australia not only look very stretched by local historical standards, they also look stretched when compared to ‘high growth‘ stocks on overseas markets – as shown in the chart below.

Australia’s high-growth stocks are the most expensive in the world

Source: Goldman Sachs

Case study: Why IML does not own Afterpay in our portfolios

Afterpay (ASX: APT) operates in the buy now, pay later space (BNPL). It allows retail merchants to offer customers the ability to buy goods and services on an instalment plan with a simple application process. Rapid customer acquisition has made the stock highly attractive to investors who believe high top-line growth is the most important determinant in valuing start-up companies. Since merging with Touch Corp in June 2017, APT has seen its share price appreciate +680%.

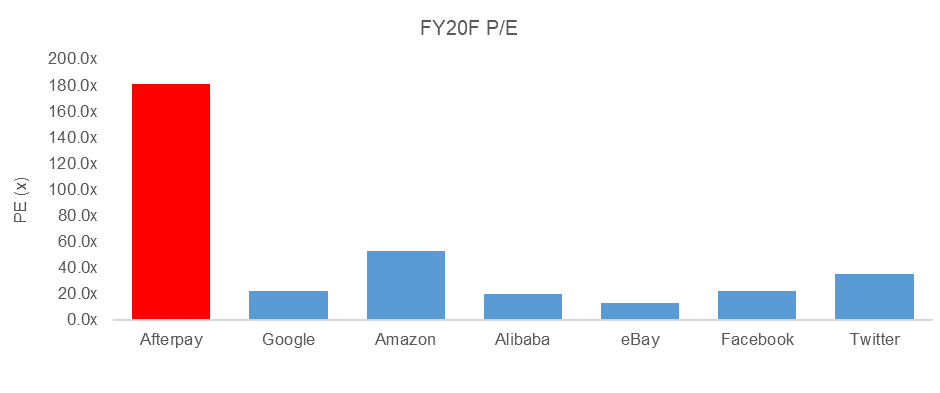

At its current share price of $24.40, APT trades on a PE of 182x consensus FY20 earnings. This is a significant premium to local rivals such as Zip and Pushpay, as well as international digital platform players such as China’s Alibaba and global giants Amazon, eBay and Google – to which it is often compared – as shown in the chart below.

Afterpay is trading well above global rivals in terms of its price-earnings ratio

Source: Factset, IML

Digital platform companies such as eBay and Google are attractive to investors because of their strong economies of scale. Once these platforms are built, the cost of adding a new user to the platform is near zero, which means that operating margins are very high. This network effect gives these platforms real barriers to entry. In contrast, Afterpay is a consumer finance company that requires capital to grow. In the past 14 months alone, APT has raised more than $450m in a mixture of debt and equity. This has been done in part to fund the company’s entry into the US and UK markets.

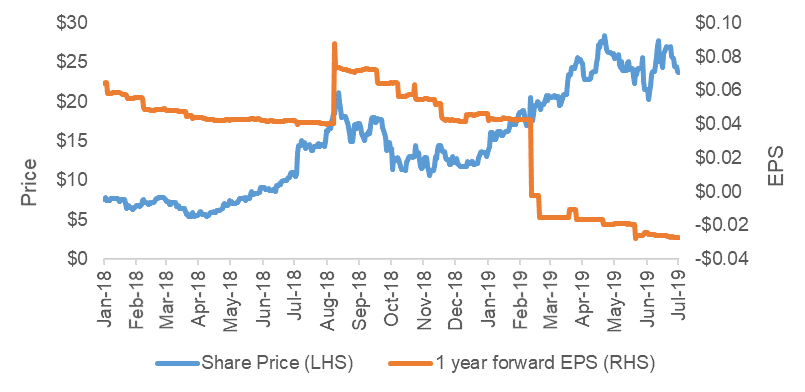

However, it is apparent that growth for Afterpay comes at a cost to both its earnings per share and returns. Despite earnings expectations for Afterpay continuing to decline, its share price has continued to rise as investors increasingly value the company on its potential blue sky, as shown in the chart below.

Afterpay’s rising share price defies dwindling earnings expectations

Source: Factset, IML

The returns Afterpay currently enjoys – albeit low – also seem likely to decline in future. APT has avoided regulations that traditional providers must abide by, but this privilege seems likely to be whittled away in future. The recently announced AUSTRAC audit into the company, for example, will increase the company’s reporting obligations in Australia, making it harder to acquire customers as quickly. Moreover, APT does not seem to us to enjoy any sustainable competitive advantage, and increased competition will erode its margins over time. The likes of Splitit, Flexigroup, Zip and Sezzle have all launched similar offerings recently. Incumbents like Visa are also entering the market which Afterpay is servicing.

Case study: Why IML owns Integral Diagnostics in its small-cap portfolios

Investors should be aware of the risks of disruption and increasing competition to incumbent players. Yet incumbency does not need to be a company’s death warrant as incumbents can better compete and increase their productivity by investing in technology and process improvements.

Radiology company Integral Diagnostics (ASX: IDX) is an example of a company that has benefited significantly from both technology advancements and network benefits.

Improvements in imaging technology means that radiologists today can diagnose far more conditions than even 10 years ago. Improvements in technology have greatly enhanced the radiology industry’s ability to detect chronic conditions such as prostate cancer and heart disease. Thanks to technological advancements and IDX’s investment in tele-radiology, the company has managed to increase its productivity with an improvement in underlying operating margins by over 200 bps since 2015. Tele-radiology is the transmission of radiological patient images, such as X-rays, CTs and MRIs, from one location to another for the purposes of sharing studies with other radiologists and physicians.

In the medium term, the introduction of artificial intelligence will also increase Integral Diagnostics’ productivity. IDX also enjoys network effects through its hub and spoke model, with hospital sites forming the hub of operations while surrounding clinics help manage patient flow. This management of patient flow helps ensure the efficient utilisation of radiologists’ time, as well as expensive diagnostic imaging capital equipment. It is also helping prevent the loss of patients to competitors. This model allows IDX to have a very commanding position in the catchments in which it operates.

In addition to these productivity improvements, IDX seems well placed to benefit from Australia’s increasing percentage of its population over age 65. This aging cohort will increasingly require higher-end diagnostic modalities such as CT and MRI scans. This shift towards high-end, higher margin modalities also plays to the strengths of Integral Diagnostics. There also remains the potential for further earnings upside from future acquisitions and the reintroduction of Medicare indexation in 2021.

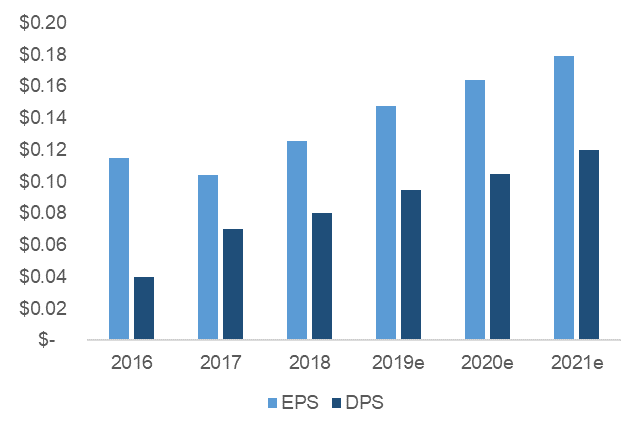

Given all the above, we expect Integral Diagnostics to grow its earnings by a compound annual growth rate (CAGR) of +12% over the next 3-5 years. At its current PE of 17x FY 2020 earnings, we believe IDX represents reasonable value given the tailwinds to its earnings, as shown in the chart below.

Integral Diagnostics’ earnings outlook is compelling

Source: IML

Conclusion

While many investors in Australia and around the world seem enamored of the upside potential of many domestic IT and other ‘high growth’ stocks, it remains clear to us as experienced investors that investment fundamentals and assessing the balance between risk and reward remain crucial when deciding whether a company is worth investing in or not.

Despite the excitement that new entrants often generate in the investment world, they are not guaranteed success and can themselves be disrupted where returns appear attractive, enticing new entrants into the market. Few will remember the excitement online search provider Alta-Vista and social media company MySpace generated when they appeared on the scene – both were labelled as amazing innovators in their time – but only a decade or two later both companies are now defunct.

While markets remain in a positive frame of mind, many investors continue to value all the potential blue sky, with current valuations playing only a minor part in their investment considerations.

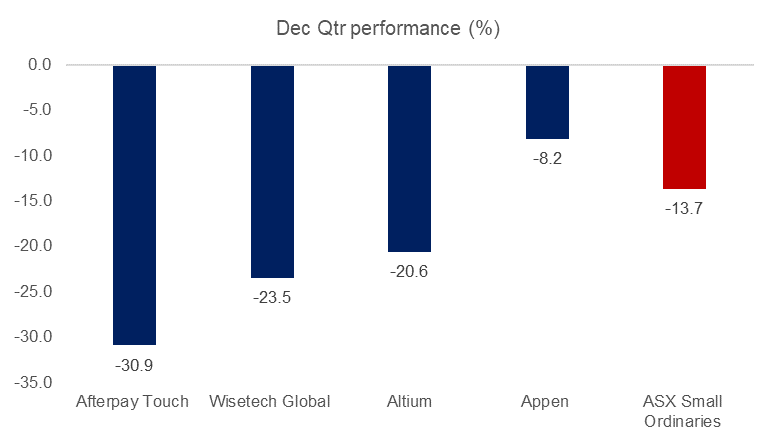

However, as we saw only as recently as the December 2018 quarter, many of these high-flying stocks can lose their allure very quickly when markets have a reality check – as seen in the chart below.

Australia’s main tech stocks had a bumpy December quarter

Source: IRESS, IML

While IML’s portfolios may lag as many investors continue to chase high-growth stocks – many of which have a very limited track record, IML remains disciplined and focused on uncovering investment opportunities and investing in companies that meet our key criteria, namely companies that exhibit:

- Strong competitive advantage with resilient barriers to entry

- High levels of recurring earnings

- The ability to grow over time

- Capable, prudent management

and which trade on what we believe is a reasonable price given the company’s prospects.

We remain confident that our investment philosophy will serve our investors well over the longer term, particularly when sharemarkets return to assessing stocks more on their fundamentals as opposed to some hoped for returns in the never never.

While the information contained in this article has been prepared with all reasonable care, Investors Mutual Limited (AFSL 229988) accepts no responsibility or liability for any errors, omissions or misstatements however caused. This information is not personal advice. This advice is general in nature and has been prepared without taking account of your objectives, financial situation or needs. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to buy, sell or hold that stock.

INVESTMENT INSIGHTS & PERFORMANCE UPDATES

Subscribe to receive IML’s regular performance updates, invitations to webinars as well as regular insights from IML’s investment team, featured in the Natixis Investment Managers Expert Collective newsletter.

IML marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected by Natixis Investment Managers Australia, on behalf of IML. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.