By Michael O'Neill

READ

2025 was another great year for equity investors, the third year in a row where the ASX 300 returned more than 10%i. All investors want the good times to keep rolling, but the longer they do and the higher valuations creep the more that nagging thought persists that an inevitable market correction is coming. Investors that want to de-risk their portfolios might be tempted to sell out, however just like a great party, you don’t want to leave too early. Time in the market is more important than timing the market, and very few investors can pick the turning points.

We think there’s another option that investors who are wary of valuations should consider – switching part of their portfolios to income-focused stocks. Long-term returns are similar, but while capital appreciation from stocks fluctuates significantly, dividends are much more resilient through the cycle.

Income is more consistent than share prices

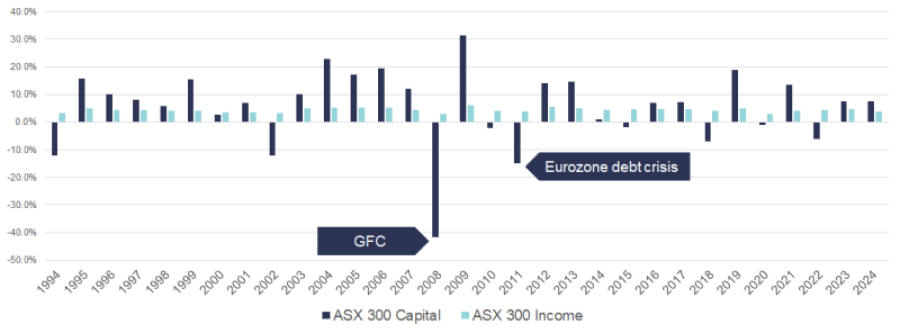

Around half of the returns from the ASX300 over the past 30 years have come from dividend income and around half from share price appreciationii. However, the way these returns have been delivered is very different as can be seen in the graph below.

Calendar year returns of the ASX 300 – capital vs income

Source : Factset, as of January 1, 2026. Past performance is not a reliable indicator of future performance

While capital returns have yo-yoed over the past 30 years dividend yields have quietly motored along at around 4-5% almost every year. Dividends are inherently less volatile than share prices as dividends are paid based on the underlying profitability of the company, whereas share prices fluctuate depending on the whims of the market. Investors can also further reduce the volatility of equities by focusing on higher-quality companies, and increase the income they receive by investing in companies that pay consistent dividends.

But getting income from dividends is harder these days

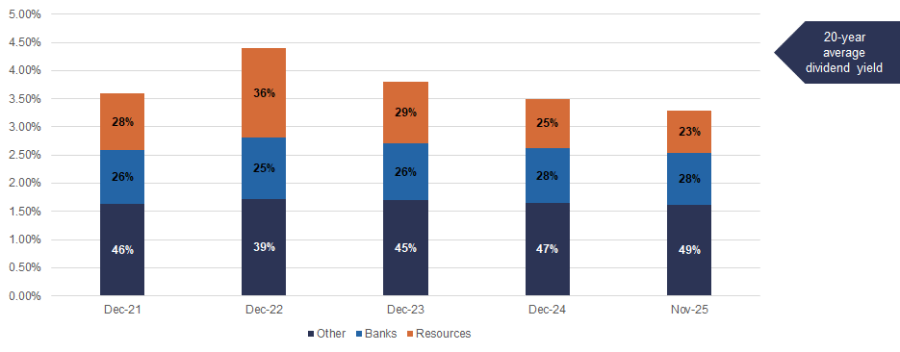

Dividends remain more reliable than capital returns, but unfortunately dividend yields have been steadily declining over the past 5 years. The dividend yield from the ASX300 is around 3.2% right now, which is down from the long-term average of 4.4%iii.

The simple reason why is that valuations are higher and dividends yields have declined. Financials and materials stocks make up around 50% of the index between them, but yields for both sectors have fallen. While financial stocks have risen significantly this year, they have outpaced growth in their earnings and dividends and so this has dragged down their yields. The dividends for materials stocks have fallen even further, particularly for the big iron ore miners.

You can clearly see in the graph below, how dividend yields have dropped from 4.5% in December 2022 (around the long-term average) to 3.2% at the end of 2025. In the past 3 years yields from financial stocks have dropped from around 5.1% to 3.8% and dividend yields from Resources stocks have fallen from around 5.5% to 2.9%iv. While the yield from banks and resources has dropped, other sectors have remained relatively consistent, and now make up a greater percentage of the overall yield.

ASX 300 forward dividend yield contribution

Source: Factset, as of 30 November, 2025. Past performance is not a reliable indicator of future performance

While dividend yields from resources and bank stocks have dropped, and yields in Consumer Discretionary and IT stocks are also low, it’s not the same story in other sectors. Utilities stocks are paying yields of 5.6% on averagev and there are also healthy dividends available in the Industrials sector. Many of these stocks also have steadier earnings, pay consistent dividends, have lower macro-sensitivity and are still trading at reasonable valuations. We like select holdings in Infrastructure and Real Estate too, though we are cautious of anything with high debt or rate-sensitive valuations and favour anything with inflation protection – for example inflation-linked price rises.

Our top three income stocks for 2026 and beyond

At IML we focus on quality and value stocks and have a strong focus on lower volatility and protecting capital when markets fall. We think that what makes a great income stock is one that is low risk, is growing its dividends, and has highly recurrent revenue and therefore dividends. In this stage of the economic cycle, with inflationary pressures again threatening, we also favour businesses that are resilient through the economic cycle, have low debt, valuations that are less sensitive to interest rates and some kind of inflation protection.

In short we want to avoid dividend traps and hold businesses where we have a high degree of confidence they will pay the dividends we expect, not just this year but also in years to come.

Here are our top 3 income stocks:

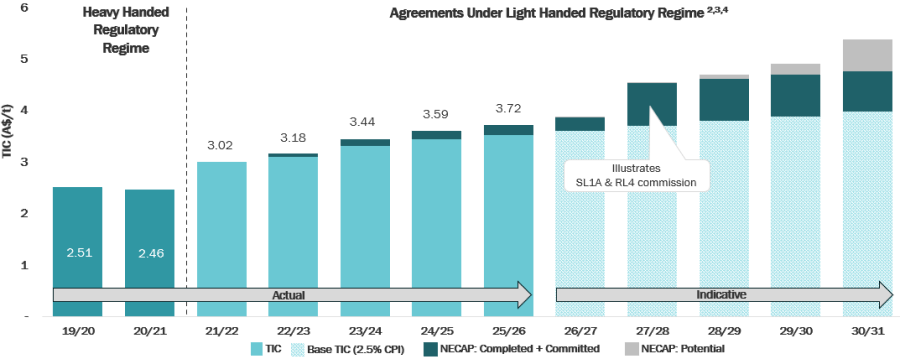

1. Dalrymple Bay Infrastructure (ASX:DBI) is one of the best assets listed on the ASX. It operates the port at Dalrymple Bay, south of Mackay in Queensland, which is a major coal export facility. It has contracts which stipulate 100% take-or-pay for the coal that runs through its ports (which means that it gets paid the same amount even if it doesn’t ship any coal). It has a long-term lease on the port to 2051 with an option to extend until 2100. The company is able to increase its prices by CPI every year and in 2031 there is even further opportunity to lift price and the business takes very little operational or capital expenditure risk.We think this chart best exemplifies the case for DBI, it shows how steadily and consistently revenue has grown since the new, lighter tough regulatory regime, and also the predicted growth in revenue until 2031, split up into three different levels of certainty:

- The light blue is relatively certain

- Green is completed and committed, so also nearly certain

- Grey is contingent on DBI being able to follow with its intended capex spend.

DBI historic and predicted growth in revenue

Source: Dalrymple Bay Infrastructure, August 2025, Half year financial results investor presentation.

1. Excludes financing costs and interest during construction (IDC). The forecast expenditure is based on P95 estimate of costs. The $405.5m is calculated as the previously reported $394m less amounts added to the NECAP Asset Base on 1 July 2025 of $28.1m (excluding IDC) plus new NECAP Series X, which was unanimously approved by customers, totalling $39.5m. Of this $405.5m, approximately $122m has been spent as at 30 June 2025 but not yet added to the NECAP Asset Base.

2. Chart is indicative only and does not represent a forecast or future outlook.

3. NECAP Projects are subject to the prudency procedures under clause 12.10 of the 2021 AU in order to be included in the NECAP Charge. NECAP is deemed prudent where it was recommended by the Operator and was approved by all customers to be incurred.

4. Figures represent TIC Year. TIC labels represent the TIC per contract tonne. DBT is fully contracted at 84.2Mtpa to 30 June 2028 with evergreen renewal options for customers. 2026/27-2030/31: Scenario is indicative only and does not represent a forecast or future outlook. Scenario assumes inflation of 2.5% p.a. (light shading); 10yr Australian Government Bond rate of 4% from July 2025, noting it is reset annually; Potential NECAP expenditure on a reasonable commissioning profile; QCA fees are included in the data but not illustrated as negligible; No 8X Project impacts included.

DBI was up nearly 50% in 2025 but we think it has room to keep going up and is paying an attractive and growing dividend.

2. Charter Hall Retail REIT (ASX:CQR) is our pick of the real estate sector. It operates neighbourhood centres around Australia which have very low vacancies through the economic cycle. These centres have great anchor tenants like Coles or Woolworths and they don’t have to spend a lot of capital to maintain their centres from year to year. The rent for many of CQR’s tenants is linked to CPI, and for others it has managed to increase rents by more than 3% in 2025, showing strong pricing power. CQR is also degearing its balance sheet, reducing its debt levels, which puts it in a good place if interest rates need to rise again.We really like this table below, which highlights the investment thesis for CQR. It shows how stable the business is with its vacancy rates, all through the economic cycle, hardly budging.

QR convenience shopping centre retail portfolio – occupancy rates

Source: Charter Hall Retail REIT 2025 Full Year Results, 18 August, 2025

CQR was up ~40% for 2025 but is still trading at a 14% discount to net tangible assets and a dividend yield of 6.2%vi, so we think it still looks reasonably priced

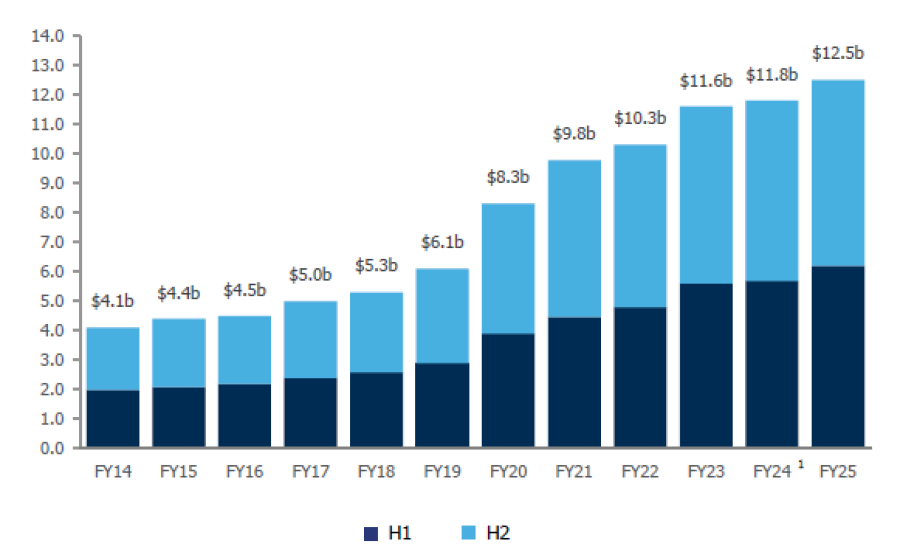

3. Steadfast (ASX:SDF) is our final income pick, and one of our favourite stocks at the moment. It’s the largest insurance broker and underwriting agency in Australia and NZ, but it doesn’t take any insurance risk itself. Think of your neighbourhood broker that has been in your community for 20 years, but is backed by an ASX100 listed company.We think insurance broking is a great industry. It’s very reliable with consistent margins and recurrent revenue through the cycle with an enviable 95% client retention rate and has been one of the only financial sub-sectors globally to grow in the aftermath of the GFC.SDF is winning share in distribution from insurers (like mortgage broking did decades ago) and is growing organically and through roll-up acquisitions. This increase in scale translates to improved bargaining power it has with insurers, so allowing it to grow its margins and earnings. Check out this chart which shows the incredibly consistent growth in insurance premiums through its proprietary Steadfast Client Trading platform, which is gaining share of insurance premiums in the small-to-medium enterprise sector.

Steadfast historical growth in gross written premiums

Source: Steadfast, FY 2025 Results Investor Presentation, 28 August 2025

1 Restated for comparison purposes, with GWP from PSC, Honan and Envestbrokers excluded from 1 July 2023.

You can buy Steadfast today at an attractive PE ratio of ~15x, as the stock has been sold off with the insurance cycle. It has a yield of more than 4% and has been growing its dividends 13.5% pa on average since 2013vii. We think it still has a long runway ahead.

We think income is a good place to be this year

We hear from many investors that they reassess their portfolios and think about the year ahead in January. It makes sense to reflect on your investments after three years of double digit returns on the ASX 300. If you’re looking to derisk your portfolio we think it’s worth considering a greater allocation to equity income. While earning good dividends from the ASX is harder than it used to be, there’s still plenty of high-quality stocks available to buy at reasonable prices that also offer good opportunities for capital growth. Stocks with reasonable valuations and good dividend yields also tend to hold up better in a market correction. Focusing on income helps you to manage the pressure of trying to time the market, and keeps you invested. You can stay in the market and enjoy the ride, but if markets drop you will still have income coming in, so are less likely to need to sell stocks to fund your lifestyle, while waiting for markets to bounce back.

i. Source : ASX.com.au, as of January 1, 2026

ii. Source: Factset, as of 31 December 2025 ASX 300 30yr Total Return is 9.1%, Income return = 4.3%, Capital return = 4.8%.

iii. Factset, as of 31 December, 2025

iv. Source: Factset, from 31 December, 2022, to 31 December 2025

v. Source: Factset, As of 31 December, 2025

vi. Source: Factset, as of 16 January, 2026, both P/E and Dividend forward 12 months.

vii. Source: IML estimates as at 31 December, 2025. Past performance is not a reliable indicator of future performance.

This publication (the material) has been prepared and distributed by Natixis Investment Managers Australia Pty Limited ABN 60 088 786 289 AFSL 246830 and includes information provided by third parties, including Investors Mutual Limited (“IML”) AFSL 229988. Although Natixis Investment Managers Australia Pty Limited believe that the material is correct, no warranty of accuracy, reliability or completeness is given, including for information provided by third party, except for liability under statute which cannot be excluded. The material is for general information only and does not take into account your personal objectives, financial situation or needs. You should consider, and consult with your professional adviser, whether the information is suitable for your circumstances. Past investment performance is not a reliable indicator of future investment performance and that no guarantee of performance, the return of capital or a particular rate of return is provided. You should consider the information contained in the Product Disclosure Statement in conjunction with the Target Market Determination, available at www.iml.com.au. It may not be reproduced, distributed or published, in whole or in part, without the prior written consent of Natixis Investment Managers Australia Pty Limited and IML. Statements of opinion are those of IML unless otherwise attributed. Except where specifically attributed to another source, all figures are based on IML research and analysis. Any investment metrics such as prospective P/E ratios and earnings forecasts referred to in this presentation constitute estimates which have been calculated by IML’s investment team based on IML’s investment processes and research. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to either buy, sell or hold that stock. Any commentary about specific securities is within the context of the investment strategy for the given portfolio.

INVESTMENT INSIGHTS & PERFORMANCE UPDATES

Subscribe to receive IML’s regular performance updates, invitations to webinars as well as regular insights from IML’s investment team, featured in the Natixis Investment Managers Expert Collective newsletter.

IML marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected by Natixis Investment Managers Australia, on behalf of IML. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.