By Lucas Goode

READ

At the smaller end of the market, where companies are less closely followed and analysed, it can often take significant announcements or newsflow to get investors to stand up and take notice of undervalued stocks. In this article we highlight three companies within our portfolios that have benefitted from recent positive announcements and outline why we continue to like their future prospects. All three are top ten holdings within the IML Australian Smaller Companies Fund.

Cobram Estate (CBO): the world’s largest vertically integrated olive oil producer guiding to strong production growth

Cobram Estate is an olive oil producer that is growing alongside the rising demand in Australia and other developed markets for high-quality olive oil. This growing demand is set against structurally falling supply out of the main olive oil producing countries in Southern Europe. As more consumers continue to turn to healthier (and better tasting) cooking ingredients, Cobram Estate is capitalising on this trend. Its strong brand and product quality allow it to charge a significant premium to commodity producers, generating EBITDA margins of around 40% in Australia.

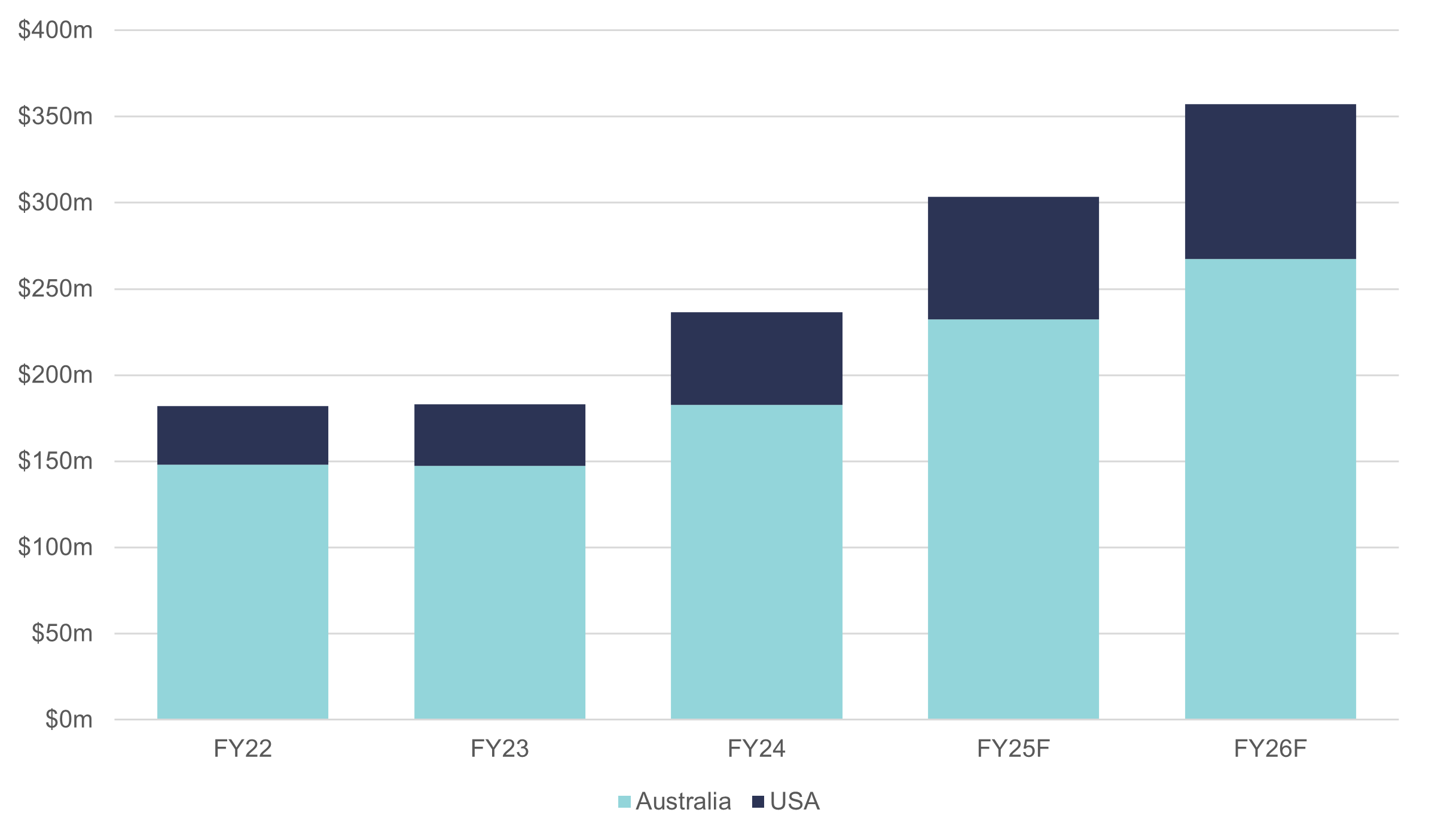

The olive oil market in the “new world” has exceptional growth potential. While the average Italian or Spaniard consumes around 10 litres a year, Australians are at less than 3 litres per person and Americans a mere 1.5 litres. This stark difference illustrates Cobram’s future demand potential, given Cobram has operations in both Australia and the United States. The company recently announced a positive Australian crop result for fiscal year 2025 and has guided to a much larger than anticipated harvest for fiscal year 2026, resulting in a healthy share price rally.

The productivity of Cobram’s olive groves are world-leading given the company’s many years of investment in agri-science and technology. Its Australian operations should benefit from capital-lite growth in the coming years as recently planted trees reach maturity and begin producing fruit. The company controls around 80% of the premium olive oil market in Australia and is already the second largest producer of olive oil in the US (which imports 97% of its olive oil). We believe it is well placed to keep growing volumes in both countries and become a great long-term success story.

Cobram Estates olive oil revenue – 2 year average

Source: Cobram Estate Olives, IML estimates, July 2025

Ridley Corporation (ASX: RIC): expanding into fertiliser

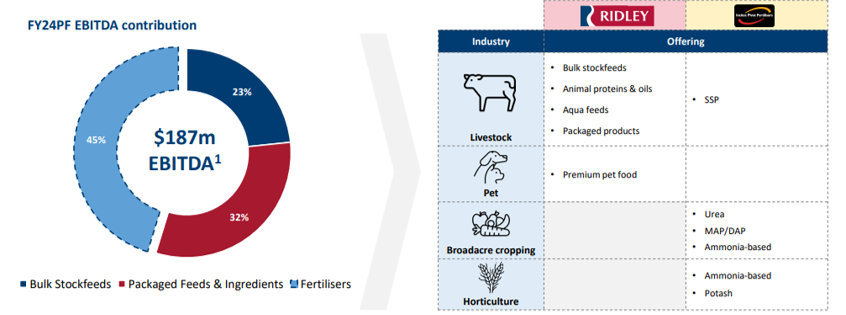

Ridley Corporation has traditionally been an animal feed manufacturer and distributor. The company has now better diversified its business after its recent acquisition of the fertiliser distribution division of Dyno Nobel. This acquisition creates a new stategic growth pillar for Ridley and allows itto tap into synergies with its existing agricultural operations. It also creates cross-selling opportunities into its existing stock feed and packaged ingredients business. We believe that the business, that has been acquired for an excellent price, will benefit under the operational focus control of Ridley, given Dyno’s singular focus on its mining explosives business in more recent years.

Ridley is a well-managed company with a strong competitive position. The management team has a solid track record of making smart, accretive acquisitions. With this latest acquisition, Ridley is well-placed to benefit across animal feed, ingredient recovery and fertiliser markets, which are expected to grow over time due to increasing global food demand. We participated in the capital raise to fund the acquisition and while the shares have performed strongly since the deal, we still view the share price as materially undervalued based on our analysis of the market opportunity for the fertiliser distribution business under Ridley’s ownership.

Dyno Nobel products have a broad range of uses and complement Ridley’s existing offering

Source: Ridley investor presentation, May 2025

Kelsian (ASX: KLS): refocusing on the core and landing new contracts

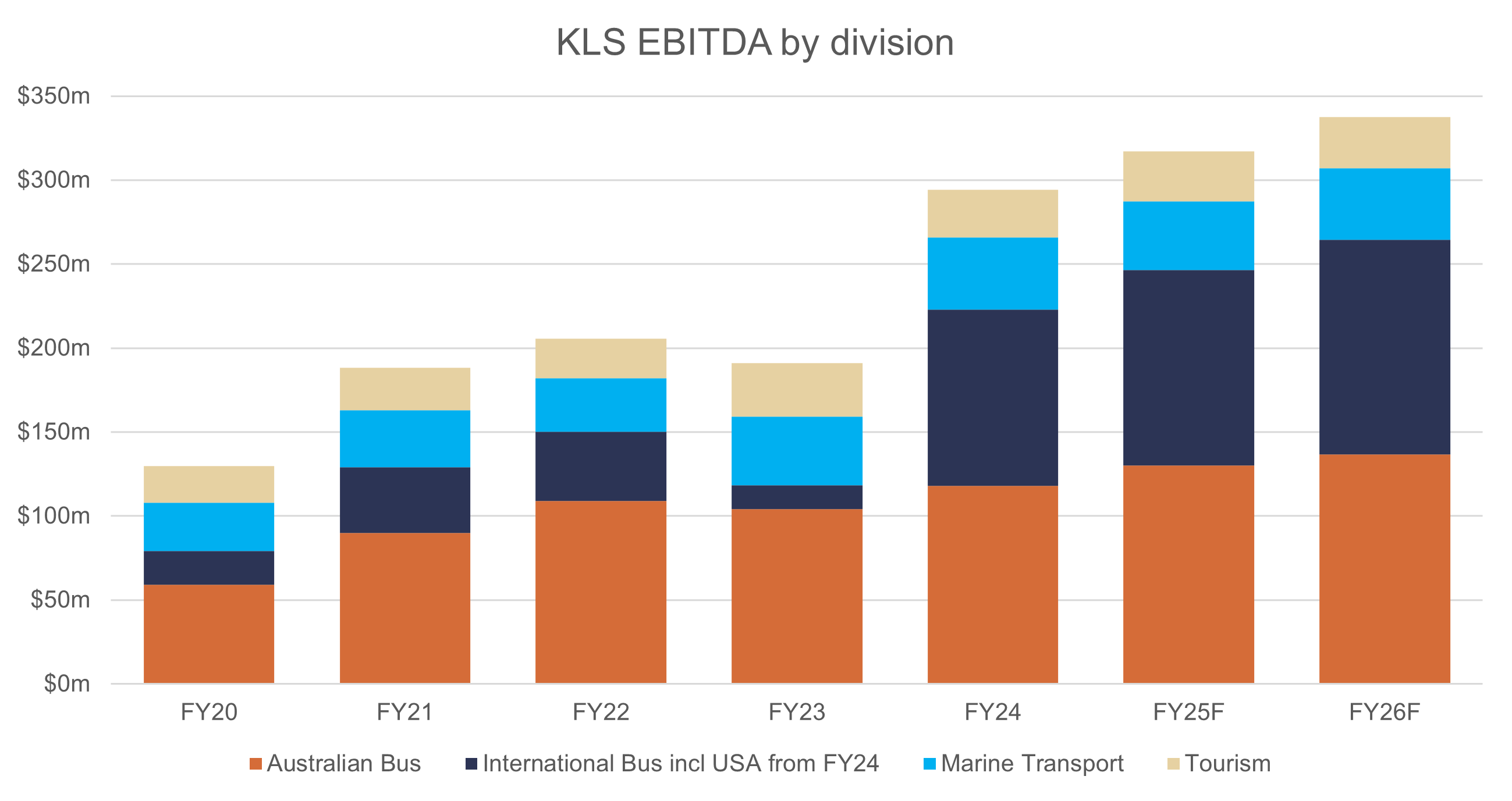

Shares in land and marine transport operator Kelsian have rallied strongly in recent months as the company announced two new large LNG construction contracts in the USA, an extension to the huge Sydney Region 6 bus contract under improved terms, and the intended divestiture of its non-core tourism operations.

We have been strongly advocating for some time for Kelsian to sell off its tourism assets, which are more volatile and capital hungry than its largely contracted infrastructure-like bus operations. It has been pleasing to see the Kelsian board reach the same conclusion. Selling the tourism assets will strengthen the company’s balance sheet and streamline its operations, positioning it for higher growth with lower capital intensity. While it has performed well recently, we continue to view Kelsian as very attractively priced at 10 times forward earnings-per-share.

Kelsian EBITDA by division

Still plenty of quality and value on offer in the smaller end of the market

The strong share price performance demonstrated by all three companies in this article in response to positive announcements demonstrates the quality and value available at the smaller end of the market where companies are often less well understood and poorly researched. We continue to find plenty of opportunities to deploy capital into undervalued small and mid-sized companies, despite the broader market being near all-time highs.

This publication (the material) has been prepared and distributed by Natixis Investment Managers Australia Pty Limited ABN 60 088 786 289 AFSL 246830 and includes information provided by third parties, including Investors Mutual Limited (“IML”) AFSL 229988. Although Natixis Investment Managers Australia Pty Limited believe that the material is correct, no warranty of accuracy, reliability or completeness is given, including for information provided by third party, except for liability under statute which cannot be excluded. The material is for general information only and does not take into account your personal objectives, financial situation or needs. You should consider, and consult with your professional adviser, whether the information is suitable for your circumstances. Past investment performance is not a reliable indicator of future investment performance and that no guarantee of performance, the return of capital or a particular rate of return is provided. You should consider the information contained in the Product Disclosure Statement in conjunction with the Target Market Determination, available at www.stg-imlimited-staging.kinsta.cloud. It may not be reproduced, distributed or published, in whole or in part, without the prior written consent of Natixis Investment Managers Australia Pty Limited and IML. Statements of opinion are those of IML unless otherwise attributed. Except where specifically attributed to another source, all figures are based on IML research and analysis. Any investment metrics such as prospective P/E ratios and earnings forecasts referred to in this presentation constitute estimates which have been calculated by IML’s investment team based on IML’s investment processes and research. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to either buy, sell or hold that stock. Any commentary about specific securities is within the context of the investment strategy for the given portfolio.

INVESTMENT INSIGHTS & PERFORMANCE UPDATES

Subscribe to receive IML’s regular performance updates, invitations to webinars as well as regular insights from IML’s investment team, featured in the Natixis Investment Managers Expert Collective newsletter.

IML marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected by Natixis Investment Managers Australia, on behalf of IML. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.