By Michael O'Neill

READ

Many market commentators love speculating on which direction markets are heading and when they’re likely to turn. But while expert speculators are loved by the media, they’re not much use to long-term investors. That’s because any experienced investor will tell you that it’s incredibly difficult to time the market – so you’re usually better off not trying. What you’re better off doing is looking at long-term fundamentals and trends and making decisions on where you’re likely to get the best return in the medium to long term.

When we look at the data, we think that now’s the time to invest in income. Why?

Capital growth in the next decade is likely to be lower than the last decade

Ultra-low interest rates and readily available, cheap, money drove a very long bull market. With high inflation and rising rates, that time has passed. While markets may, or may not, perform well in 2023, what is very unlikely is that we’ll enter another long bull market with a similar amount of capital growth.

Rising interest rates are driving down company earnings and company valuations. And central banks in the US, Australia and elsewhere are adding further macro-economic headwinds by continuing to remove money from the economy via quantitative tightening. These factors are likely to drive lower capital growth in the medium term and it’s unlikely to be a smooth ride. Volatility is also likely to remain elevated in the near term. While this makes it a challenging market for investors, it does also offer opportunity. With company valuations fluctuating it’s a stock pickers’ market, with a great chance to pick up high-quality companies at bargain prices.

For us, with capital growth likely to be lower in the medium-long term, it’s the right time to place greater focus on income.

There are different ways to generate income from an equity portfolio. In IML’s Equity Income Fund we use three main streams for income: dividends, options and capital gains. We use simple options strategies to generate around 2% income yield from the portfolio – it tends to be a bit higher in flat or bear markets. We also generate up to 1% through realising capital gains – this is higher in bull markets, but we make sure we leave room for capital growth so investors can keep pace with inflation. And then we generate around 4% income yield through dividends. This diversity of income sources tends to give us a higher, and steadier, income stream paid quarterly. At the core, we still look to dividends from low-risk industrial stocks to generate the bulk of the income.

Dividends are likely to make up a greater share of total return than capital growth over the next decade.

For us, dividends have always been an important part of investment returns, but at times like these, their importance increases. There are two main reasons why:

- Dividends provide more reliable returns than capital gains

- Dividend yields can act as a ‘safety net’ at times of volatility

1. Dividends provide more reliable returns than capital gains

Returns from a share portfolio come from two sources – the capital appreciation from the shares, as well as the dividends received from each share. If you look at the table below, showing returns from the ASX 300 over the last 20 years, you can clearly see how important dividends are to overall returns.

Over the last 20 years, dividends have returned 51% of overall returns. While this figure alone is evidence enough of dividends’ importance, it becomes more striking when you look at the volatility of these returns.

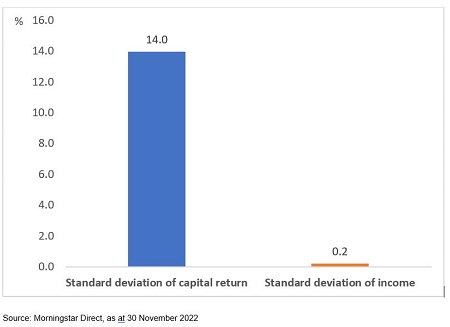

Volatility of returns of capital and income of the ASX 300 over 20 years

As you can see, return on capital fluctuates significantly, but dividend returns are remarkably reliable – making them particularly valuable when returns on capital are low, or negative.

While the level of capital returns from a share portfolio depends on movements in individual share prices, this is not the case for dividends. That’s because the level of dividends received by an investor is decided by the company’s board and is generally a reflection of the company’s overall profitability – its financial performance. So, in periods where the overall sharemarket goes down, an investor’s dividends should stay much the same if they have a diversified portfolio made up of quality companies.

2. Dividends can act as a ‘safety net’ in times of volatility

The movement in the sharemarket – particularly over shorter time periods of 6 to 12 months – is more often than not dictated by investor sentiment. Sentiment can be erratic, impacted by anything from predictions of future levels of economic activity, to inflation and interest rates, or perceptions of geopolitical stability.

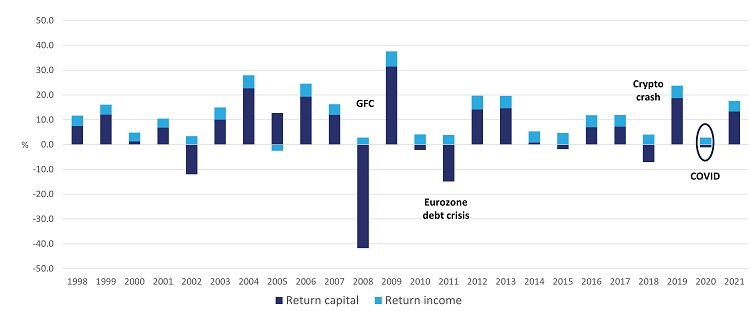

Take a look at this chart of ASX 300 returns over the last 20 years with the light blue bars showing dividends and the dark blue bars showing capital growth.

ASX 300 returns capital vs income

Source: IML and Morningstar Direct, S&P ASX300 01/01/1998 – 31/12/2021

You can see how important dividends were during those years where the ASX dropped significantly, or capital returns were lower. In the peak of the Tech Wreck in 2002 the ASX 300 provided a return on capital of -12% but dividends returned 3%.

- In 2008, at the start of the GFC, capital dropped -42% but dividends returned +3%

- In the 2011 Eurozone debt crisis capital returned -15% but income returned +4%

And while the sharemarket recovery from COVID was very swift, the ASX 300 still dropped -1% but income? It returned a steady 3%.

When the mood of the market is negative, stocks can fall heavily as investors and traders reduce their overall level of sharemarket exposure by rapidly selling shares – indiscriminately and independent of their quality. What we have observed over many years of investing is that once sentiment starts to turn, companies with sustainable earnings that support a healthy, consistent dividend stream are often the shares that recover the most quickly.

The reason for this is simple – rational, long-term investors are always attracted to companies that pay a healthy dividend from a sustainable earnings stream. They understand that the level of returns from dividends are not dependent on future share price performance. In other words, once shares in quality companies fall to a level where the dividend yield is attractive and sustainable, long-term investors buy them so they can ‘lock in’ high income levels, whatever happens to the sharemarket in future.

Which stocks and sectors are likely to pay the best dividends in future?

With the economic outlook uncertain and lower growth and high inflation likely to stick around for a while, it’s a good time for investors to think seriously about where they are likely to get the best income for the medium to long term. Investors should be cautious of overconcentrating in riskier sectors such as commercial property, resources, and other cyclical sectors.

In general, we prefer industrials for long-term, consistently high dividends. We are also looking at which sectors and stocks are likely to perform well, and so provide a steady or growing dividend, in a high inflation environment. The types of companies that tend to perform well when inflation is high are companies:

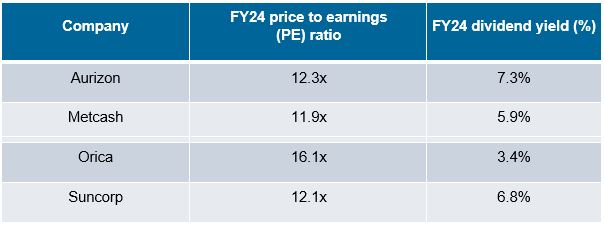

- With pricing power – their strong market position gives them the ability to pass on rising costs to their customers e.g. home and motor insurance companies like Suncorp (SUN).

- In a rational industry – the main players are motivated by profit and act ‘rationally’ to maximise long-term profits – not spending large amounts of capital at the top of the cycle, or chasing market share at all costs through unprofitble discounting. The explosives industry for example has rationalised significantly and is at a strong point in the capital cycle, benefitting companies like Orica (ORI).

- That sell essential products and services – people need to buy them, no matter how high prices go e.g. consumer staples companies like Metcash (MTS).

In addition to the above, companies need to have capable, proactive management that can put well-structured contracts in place that make difficult conversations about passing on inflationary costs easier. Ideally, contracts are structured with adjustments for inflation and pass-through of essential input costs such as fuel. Aurizon (AZJ) benefits from such contractual protections. Here are some good examples of these types of companies, which also pay high dividend yields, and are currently trading at reasonable valuations:

Source: IML and Factset estimates, 14 December, 2022

Finally, it’s worth bearing in mind the types of companies that benefit directly from rising rates. Good examples right now are Suncorp (SUN) through its investment earnings and Aurizon (AZJ) through the return determined by the regulator on its regulated asset base.

Dividends are always important, right now they’re critical.

In Australia, dividends always make up a significant part of sharemarket investors’ total return. During volatile times, down markets or protracted periods of lower capital growth then the dividend share of total returns is even higher. Nobody can, reliably, pick the bottom of the market, or know how the sharemarket will perform in coming months and years.

So in times like these, with volatility high and lower-growth likely for the medium to long term, it’s best to minimise your risks and invest your money where you have the best chance of healthy returns. For us that means buying and holding shares in quality industrial companies, at attractive valuations, that pay strong dividend yields. This has you well positioned for whatever mood the sharemarket happens to be in.

While the information contained in this article has been prepared with all reasonable care, Investors Mutual Limited (AFSL 229988) accepts no responsibility or liability for any errors, omissions or misstatements however caused. This information is not personal advice. This advice is general in nature and has been prepared without taking account of your objectives, financial situation or needs. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to buy, sell or hold that stock. IML is the responsible entity for the Investors Mutual Equity Income Fund. A Product Disclosure Statement (PDS) and a Target Market Determination are available on www.stg-imlimited-staging.kinsta.cloud. Potential investors should read the relevant PDS before deciding whether to invest, or continue to invest, in the Fund. Past performance is not a reliable indicator of future performance. Any forecasts referred to in this article constitute estimates which have been calculated by IML’s investment team based on IML’s investment processes and research.

INVESTMENT INSIGHTS & PERFORMANCE UPDATES

Subscribe to receive IML’s regular performance updates, invitations to webinars as well as regular insights from IML’s investment team, featured in the Natixis Investment Managers Expert Collective newsletter.

IML marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected by Natixis Investment Managers Australia, on behalf of IML. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.