By IML Investment Team

READ

Over the past six months, there has been a significant increase in the level of corporate activity in the Australian sharemarket. This has included takeover approaches for Spark Infrastructure, Crown Resorts, Tabcorp’s wagering division, Sydney Airports, Vitalharvest, Australian Pharmaceutical Industries and a number of others.

Companies have also been able to divest assets at much better than expected prices. Telstra, for instance, recently announced the sale of 49% of its mobile tower network ‘InfraCo Towers’ to a consortium for A$2.8 billion or 28 times earnings before interest, taxes, depreciation, and amortisation.

This article seeks to explain why this is happening, what it means for a number of companies in IML’s portfolios, IML’s approach to corporate activity, and why IML’s portfolios are well-placed to benefit from these trends.

Favourable environment for corporate activity

Government and central bank responses to the COVID-19 pandemic have created a window of opportunity for many corporates and strategic buyers to execute on their long-held M&A ambitions, or to realise significantly higher proceeds from divesting assets.

A well-executed acquisition can bring scale, integration benefits, and new capabilities which can strengthen a company’s future earnings and improve its competitive position in its industry. Ultra-low interest rates also make the economics of using debt to partially or fully fund an acquisition more potentially favourable.

With the return on risk-free assets essentially zero, and the cost of borrowing long-term debt so low, the incentive for many corporates and private equity players to acquire high cash-generating businesses using high amounts of low-cost debt is very strong. The high levels of government, corporate and household indebtedness also means that it is unlikely the cost of debt will rise significantly any time in the near future, despite current concerns about inflation.

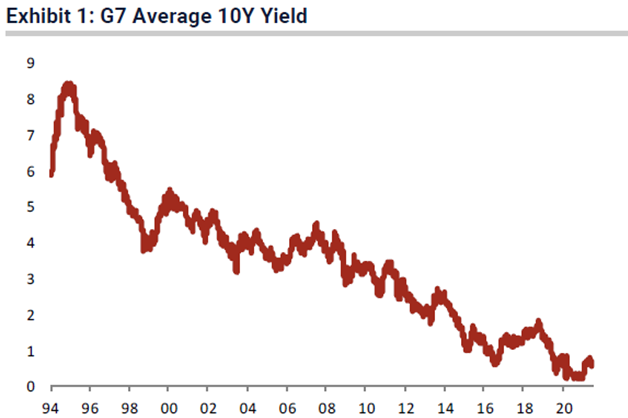

Longer-term government and corporate bond yields have fallen substantially over the past three decades. Chart 1 below shows the decline in G7 country average 10-year government bond yields over this period. With rates and returns so low, there is a propensity for investors to take on more risk as they seek higher returns. As a consequence, even higher-risk assets such as corporate ‘junk’ bonds are generating returns below inflation.

Chart 1: Decline in G7 Average 10-Year Government Bond Yields, 1994 – 2021

Sources: Bloomberg, Jeffries

In addition to the tremendous amounts of government and central bank stimulus, notwithstanding the short-term lockdowns at the time of writing, the accelerating rollout of vaccines for the COVID-19 virus is likely to mean that the economic outlook in many regions is likely to normalise over the next 12-18 months. Similarly, the cashflows for most companies in IML’s portfolios are already either stronger than they were a year ago or are expected to continue to improve significantly going forward.

Sharemarket activity has been very momentum-driven, fixated by news flow and trading updates which have continued to push many companies’ share prices higher. In this environment, companies which have been affected badly by COVID-19 lockdowns and which are still recovering to their pre-COVID earnings levels have lagged the broader market rally. With interest rates so low and many companies’ shares still trading at relatively lower levels than when interest rates were higher, acquirers have the opportunity to buy businesses at attractive prices if the market does not recognise the long-term value on offer.

Opportunities for acquisitions

In this environment, we expect a number of companies in our portfolios to make acquisitions which will be earnings-accretive, which will allow the business to increase scale and further strengthen competitive advantages, expand market share, and ultimately enable the company to grow its business faster over time.

• Amcor (ASX: AMC) is one of the largest global packaging suppliers, has a strong balance sheet, and is using its strong cashflows to undertake a US$350 million share buyback.

• CSL (ASX: CSL) is the clear global leader in plasma/blood products, has a track record of making astute and sensible acquisitions over its history, and as a result, has been able to generate consistently higher returns than many of its competitors.

• Orica (ASX: ORI) is the largest explosives player in the world with a unique network of plants. Orica is completing the integration of Exsa, Peru’s leading manufacturer and distributor of industrial explosives, establishing Orica as the number one player in Latin America. Further acquisitions, in conjunction with Orica’s investment in research and development and technology to drive the development of new products, will enable Orica to generate stronger earnings growth and grow its market share further.

• Sonic Healthcare (ASX: SHL) is a pathology company which has undergone significant global expansion over the past 20 years, and has also been expanding its radiology footprint in Australia. The strength of Sonic’s cashflows, combined with the company’s extremely low debt, means that the firm’s balance sheet is in its healthiest state in 20 years. This puts Sonic in a much better position than many of its smaller or more leveraged competitors, and we expect Sonic’s highly-capable and experienced management team to make further earnings-accretive acquisitions.

All the companies above have expanded their global footprint in the last 20 years through a number of often well-timed acquisitions and continue to be actively on the lookout for bolt-on acquisitions around the world.

Potential takeover targets

Since our inception in 1998, IML’s investment philosophy and approach has been to invest in companies which we believe possess a strong, sustainable competitive advantage, which generate recurring earnings and which are managed by what in our view is a capable management. We also like companies with these characteristics that have a viable long-term path to growing their earnings and which in our view are trading at a reasonable price.

Given this, it is not surprising that many of the companies we own are frequently attractive either to other publicly listed companies or to private equity players, and our portfolios are well-placed to potentially benefit from future corporate activity. A number of the companies we own are already the subject of corporate activity, including Australian Pharmaceutical Industries, Spark Infrastructure and Tabcorp.

The following is a selection of companies we own in our Funds which are already or which we believe are likely to be attractive to corporate players as their share prices look undervalued given the position of each company in its respective industry.

Australian Pharmaceutical Industries (ASX: API)

Australian Pharmaceutical Industries (API) recently received a bid from Wesfarmers at $1.38 per share. Wesfarmers has clearly been attracted to API’s strong position within the in-demand health and wellness industry. API’s stable, cash-generative wholesale pharmaceutical distribution division provides a solid platform enabling the company to invest in its growing Priceline national franchised pharmacy network and Clear Skincare Clinics beauty treatment business.

API has several significant long-term upside opportunities. The company is the number two player behind Chemist Warehouse in a fragmented retail pharmacy sector, and is adding 10 – 15 pharmacies to its network each year. We believe that over time, an increasing number of independent pharmacies will find it difficult to remain viable businesses, which should enable API to attract more pharmacies to Priceline, increasing the earnings from this division.

One of the ‘hidden gems’ that we believe the market has not recognised is Priceline’s seven million member ‘Sisterhood’ loyalty program. This gives API valuable opportunities to market offers and discounts to Priceline customers, driving bigger basket sizes (the number of items sold in a single purchase) and more repeat business. The loyalty program also represents a strong opportunity to cross-market Clear Skincare Clinics products and services to what is an overlapping customer base.

Insurance Australia Group (ASX: IAG)

Insurance Australia Group (IAG) is the largest general insurance company in Australia and New Zealand, and owner of the iconic NRMA brand. IAG provides personal insurance products such as home and motor insurance as well as commercial insurance. IAG operates in a highly consolidated market and holds close to 30% market share alongside Suncorp. IAG’s competitive advantage lies in its trusted brands such as NRMA and CGU and its scale, which gives IAG access to low-cost repair networks.

IAG’s personal lines insurance business is highly-profitable, earning returns in excess of 15%. The commercial insurance business, like that of peers, has however been affected by COVID-19, predominantly because of business interruption insurance. This led IAG to take provisions in excess of A$1 billion and raise A$776 million in equity in the depths of the initial COVID-19 pandemic onset in 2020.

Given that business conditions are expected to recover, these provisions now appear excessive, and are likely to be at least partially written back. This will mean that IAG’s capital position and balance sheet will be extremely robust. In addition, the outlook for IAG’s insurance businesses is also very favourable, as the industry is acting rationally by lifting premiums (prices), and focusing more on profitability than market share gains following a tough year in 2020.

All this means that it would not surprise us if there was an opportunistic bid from an overseas insurance company looking to expand into Australia. It is worth mentioning that Berkshire Hathaway purchased a A$500 million stake in IAG back in 2015 at A$5.57 a share.

Incitec Pivot (ASX: IPL)

Incitec Pivot is a diversified chemicals company which manufactures and distributes explosives and fertilisers. It is the largest explosives company in the United States and the largest fertiliser manufacturer and distributor in Australia. The firm’s competitive advantage is the privileged locations of its plants and distribution assets near its customers and its access to low-cost inputs.

After having undertaken significant capital expenditure in recent years on improving the manufacturing performance of its plants, Incitec Pivot is now ex-capex, generating strong cashflows, and currently benefitting from very high fertiliser prices. The company will also benefit in the years ahead from the US Government’s trillion dollar planned infrastructure spending, which will lead to strong demand from Incitec Pivot’s quarry and construction customers in the US.

Incitec Pivot also has a strong balance sheet and a very appealing valuation, particularly given the high multiple the fertiliser distribution business in Australia could attract from other industry players. This could make Incitec Pivot a target for an industry competitor such as Wesfarmers, which could potentially achieve significant synergies from such an acquisition, or from private equity players which could look to break the business up and sell it in parts, thereby achieving much higher multiples than where Incitec Pivot is trading today.

SkyCity Entertainment (ASX: SKC)

SkyCity Entertainment owns strategic assets which are hard to replicate. The predominant asset, the Auckland casino, has the license to operate in the centre of New Zealand’s largest city. SkyCity also owns a significant parcel of land surrounding the casino complex upon which the firm operates several hotels and a range of food and beverage operations. SkyCity also owns and operates the Adelaide casino, also in the CBD, which has recently been expanded and upgraded with the addition of a hotel.

SkyCity has invested about A$1 billion over the past six years to construct two new hotels and a convention centre and to expand its gaming facilities. This programme of work is nearing completion, and the new assets will start to contribute to earnings in coming years. Free cashflow generation will also increase significantly as SkyCity will no longer need to fund major capital expenditure.

Government lockdowns and the absence of overseas high roller players have affected SkyCity’s recent earnings performance. As restrictions on physical movements reduce, company updates have shown that earnings have the ability to recover quickly, with local gaming proving very resilient. We believe SkyCity’s current valuation does not reflect the company’s significant investment over the past six years and increased earnings potential. If the market does not rerate the share price, in our view we would not be surprised if SkyCity becomes a target for a corporate acquirer, particularly in light of the company’s significant land holdings.

United Malt (ASX: UMG)

United Malt is one of the largest malting companies in the world and is the only listed player in the industry. United Malt is a relatively new listing to the ASX having been demerged from Graincorp. United Malt was demerged in early 2020 partly in reponse to several buyout proposals that Graincorp had received for the company.

The company owns and operates 12 processing plants and a network of 21 distribution warehouses across North America, the United Kingdom, and Australia. These malting plants are strategically located close to barley-producing geographies and to brew houses or distillers that require a steady supply of malt to manufacture beer and whiskey. United Malt also services the fast-growing US and Australian craft beer markets, supplying a range of malts along with other products and services. Scotch whiskey production is also growing on the back of strong demand for pure malt whiskeys.

United Malt’s earnings were affected by the lockdowns implemented over the last 12 months, with on-premise consumption hitting the firm’s craft beer customers particularly hard. As lockdown restrictions are easing in most parts of the world, on-premise volumes are returning to more normal levels as demand for beer particularly from craft brewers increases and this is generating an improved outlook in demand for malt.

The longer-term outlook for craft beer remains positive as consumers switch to the fuller flavours of craft brews, which should underpin demand growth in United Malt’s brew services division. The company is also in the middle of a transformation program expected to deliver A$30 million in savings over the next three years through improved warehouse utilisation, production enhancements to processing plants and route optimisation.

Given these forthcoming improvements and given previous corporate interest in the company, it would not be surprising if United Malt attracted takeover interest, given the entrenched market position of each of the firm’s plants, the company’s fairly predictable cashflows, and the growth opportunity offered by craft brewery and whiskey distilling. Similar companies have traded at higher multiples in the private market than United Malt currently trades on. With interest rates so low, the predictable cashflows United Malt produces would be attractive to a cashed-up acquirer. Further, we believe United Malt may be attractive to private equity players on the basis that each region could be sold separately to an in-market operator which could extract significant synergies when acquiring United Malt.

IML’s approach to corporate activity

Over the years, we have been a significant shareholder in a number of companies which have been the subject of corporate activity. These have included Energy Developments, Recall, Tox Free Solutions, Vitalharvest, and numerous others.

In our previous article When being an active shareholder can make a difference, we discussed how on behalf of the investors in our Funds, we often exercise our right as the part-owner of businesses to hold Boards and managements accountable to their shareholders. We take this responsibility very seriously, and it underpins how we respond when a company in which we are invested is subject to a takeover offer, or plans to divest part of its business.

Investment bankers make their living by pitching often ingenious and attractive propositions for corporate activity to Boards and management teams. As an active investor, it is our job to ensure that any such activity maximises long-term value for all shareholders, including investors in our Funds. There have been a number of occasions in the past when we have argued forcefully against proposed corporate actions where we believed that this was not the case. (An example was IAG’s proposed acquisition in 2015 of a Chinese insurance company, which subsequently did not proceed.)

Conclusion

As we have outlined above, a number of the companies in our portfolios are likely to attract corporate interest in the coming months and years, providing an opportunity for investors in our Funds to benefit from exiting our shareholding at a premium to the prevailing share price.

Alternatively, many companies that we own and which have been expanding overseas are likely to take advantage of the current low interest rates to make accretive add-on acquisitions which should help strengthen their operations by increasing their scale and competitive advantage, and which should enable these companies to accelerate their long-term earnings growth going forward.

At IML, we continue, as we have done since 1998, to put significant time and effort into analysing the potential corporate activity and engaging with companies to ensure that any such activity is in the best interests of investors in our Funds. This process should continue to contribute to our Funds’ ability to deliver sound returns to our investors.

While the information contained in this article has been prepared with all reasonable care, Investors Mutual Limited (AFSL 229988) accepts no responsibility or liability for any errors, omissions or misstatements however caused. This information is not personal advice. This advice is general in nature and has been prepared without taking account of your objectives, financial situation or needs. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to buy, sell or hold that stock. Past performance is not a reliable indicator of future performance.

INVESTMENT INSIGHTS & PERFORMANCE UPDATES

Subscribe to receive IML’s regular performance updates, invitations to webinars as well as regular insights from IML’s investment team, featured in the Natixis Investment Managers Expert Collective newsletter.

IML marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected by Natixis Investment Managers Australia, on behalf of IML. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.