By IML Investment Team

READ

Technology stocks around the globe have performed exceptionally well in recent years, led by US success stories such as Facebook, Apple, Amazon, Alphabet, Microsoft and Cisco Systems. These companies are well established, profitable, cashed-up tech leaders with formidable business models and a well-recognised global presence.

Australia’s tech sector has also been caught up in this trend so that companies like WiseTech, Nearmap, Afterpay and Zip Co, have all soared in value. Stocks such as these are now collectively valued at tens of billions of dollars despite their largely unproven business models.

It is fair to say that an investment in Australia’s tech companies is a very different proposition to investing in the US tech companies listed above. These locally listed stocks have in most cases neither the track records nor global reach to justify their current valuations and, as such, they are not held in IML’s portfolios.

Having said this, when researching our companies and assessing their outlooks, technology and innovation remain an essential part of what we look for in any company. In fact, apart from being well-established companies that have proven business models, the positive outlook for many of the industrial companies held in our portfolios is due in part to technological innovations that these companies are embracing which will help these companies grow their earnings in years to come.

In this article, we detail a few examples of stocks that we own where the use of new technology is an important part of why we have positive outlooks on these companies.

Tabcorp

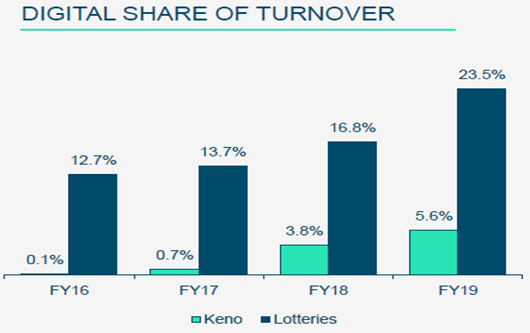

Tabcorp operates all the lottery licences in Australia (except WA), enabling the company to run a series of lottery games every week throughout the country. While the sale of ‘scratchy’ and paper lottery tickets remains an important part of this business, we expect Tabcorp’s lotteries’ business to be a significant beneficiary in the years ahead from customer migration to its digital platforms. Revenue in Tabcorp’s lotteries business has recently begun to grow strongly as it connects more of its customers to its new digital lotteries platform.

It is interesting to note that customers who use Tabcorp’s digital lotteries platform spend 52% more on average than customers who pick up their lottery tickets from a retail store, such as a newsagent or convenience store. In addition, direct digital customers are margin accretive to Tabcorp as there is no need to pay and commission to re-sellers. For example, in NSW and Queensland Tabcorp pays a commission rate of 9% to newsagents on the value of their lottery ticket sales.

By using its digital channels, Tabcorp is also able to have a more focused and cost-effective means of promoting upcoming lotteries to its customers than via traditional media. Currently, only 24% of Tabcorp’s lotteries turnover is earned through its digital platforms, and we expect this percentage will rise materially higher over the next 5 years as has happened in other countries. For example, in Finland, digital lottery penetration is now at 48%.

Lotteries’ digital share of Tabcorp’s turnover

Source: Tabcorp FY19 results presentation as of 30 June 2019

In FY19, lotteries made up 48% of Tabcorp’s earnings before interest, tax, depreciation and amortisation (EBITDA). We see lotteries growing consistently as retail customers transition to Tabcorp’s digital platforms, and we expect the lotteries division to grow steadily over the next few years.

Orica

Orica is the world’s largest explosives company which derives the majority of its earnings from ammonia nitrate plants located in many countries worldwide. Orica’s market-leading position and global scale make it an investment worth considering for most long-term, prudent investors such as IML.

One of the main reasons we hold Orica across our portfolios is its heavy research and development (R&D) into wireless blasting systems, as well as its other leading software development. The success of these innovations gives us confidence in Orica’s earnings outlook in the next 3 to 5 years.

Orica’s valuation multiple is similar to the typical traditional industrial company. Yet, after years of R&D investment, the company has recently developed the world’s first wireless detonation device which we believe – following many discussions that we have had with Orica’s mining customers – will revolutionise mining and mine plans into the future.

The wireless detonation device will replace the current explosive systems used by all mining companies that uses wires and manual blasters. The use of Orica’s new wireless detonation system will lead to much greater safety and much higher productivity for Orica’s customers. We believe Orica’s wireless detonation systems and huge R&D innovation will help Orica increase its market share and margins in the years ahead. In our view, these increases will underpin the company’s earnings growth over the next few years.

Orica’s wireless detonator improves safety and productivity

Source: Orica presentation; May 2017

Coles

Coles is another well-established industrial company that we believe will benefit materially from the use of new technologies that it is introducing.

Under Wesfarmers control, Coles had improved its earnings mainly from a complete repositioning of its product range as well as from an intensive store refurbishment programme. Throughout this period, the company underinvested in its supply chain and distribution centres (DCs), with Coles’ distribution network made up of a patchwork of poorly located, labour-intensive, sub-scale and dated sheds.

Following its demerger from Wesfarmers and listing in late 2018, IML accumulated shares in Coles at what we believed were very attractive prices. The company looked particularly attractive to us as we believe Coles is set to benefit greatly from the company’s investment in new technologies to automate much of its current distribution chain.

Coles’ new management team – which has been in place since the listing – has made it a priority to increase the efficiency of the group’s distribution network. As a result, Coles has announced the investment of nearly $1bn in the next three years to adapt new warehouse automation technology from WITRON in the group’s two planned, state-of-the-art DCs in Sydney and Brisbane. The new DCs will replace a large number of Coles’ smaller DC sites spread all over the country, which will lead to significant cost savings and efficiencies for the group.

Coles current inefficient supply chain network

Source: Demerger of Coles scheme booklet as of 21 Nov 2018

Automation will allow for fully automated picking of stock for each individual store. The new systems being implemented in the new DCs will also allow for the stock to be loaded into trucks at the DC in the most efficient order for unpacking on arrival. In addition to obvious efficiencies, this will also allow Coles the ability to customise stock for individual stores based on specific local demographics, which we expect will also help improve sales across its store network.

In addition to the new DCs, Coles is also investing heavily in its online offering by doubling its delivery capacity through technology from Ocado, a global leader in online shopping technologies.

In 2-3 years, Coles will launch a new website, which is planned to be far more user friendly, which will make automated suggestions based on algorithms, including a recipe function which would allow customers to order all ingredients for a given meal, such as tacos, with a single click.

Orders placed online will also be fulfilled from better located, smaller and more local DCs, which will also be highly automated. This will ensure fewer instances of running out of stock, which tends to occur when online orders are packed ‘in-store’. In addition, software technology will ensure drivers take the fastest, most cost-effective delivery routes.

We expect all of the above factors to lead to a significant improvement in customer experience, as well as improved sales growth and lower costs for Coles. It’s a potent combination and while the shares have been significantly rerated since our initial purchase we continue to hold shares in Coles as we have confidence in the company’s earnings outlook over the next 3 to 5 years.

Steadfast

Steadfast is an industry leader in insurance broking and underwriting across Australia, with a network of 398 broker businesses and 26 underwriting agencies which generate total billings of $8.4 billion per annum as of 30 June 2019.

The company, founded in 1995, has a track record of steadily increasing market share and improving cost efficiency. Over the years, its growth has come largely from low-risk, bolt-on acquisitions and organic growth.

However, since its 2013 ASX listing, Steadfast has invested more than $80m in IT systems and processes. This size of the company’s IT investment now gives it a very strong competitive advantage against peers and underpins its potential for further market share gains and cost savings. For example, its gross written premium (GWP) transacted through its Steadfast Client Trading Platform (SCTP) has nearly doubled in the year to 30 June 2019 to $440m as shown in the chart below.

Source: Steadfast FY19 earnings results presentation as of 17 Oct 2019

This is only the tip of the iceberg in our view. We see 60% of the total Steadfast Network GWP transacting through SCTP in the next four years.

More than 300 brokerages are currently using SCTP, with eight business lines as well as 13 insurer and underwriting agency partners live on the platform, including Allianz and Berkley. The platform will gradually incorporate a suite of insurance products across six major insurers, delivering revenue, market share and cost efficiencies for Steadfast and its brokers.

Steadfast’s recent successful bid for Insurance Brokers Network Australia (IBNA) creates the potential to add another 79 IBNA brokerages and about $1.25bn in GWP to the company’s network, expanding its potential SCTP user base.

Also, in the current post-Hayne Royal Commission environment, SCTP delivers strong client outcomes. For example, Steadfast has removed barriers to broker and insurer adoption of SCTP. From a client-service perspective, this helps ensure brokers have the smoothest possible access to Steadfast’s best-policy wording and compliance management.

In addition, we expect Steadfast’s INSIGHT, a client-relationship management and back-office system, to become the new system of choice for brokers in management of the entirety of their business. At present, 112 brokerages are using INSIGHT, with more than 2,500 licenced users. An additional 34 brokerages have committed to migrate onto INSIGHT. Steadfast is in discussions with a further 88 brokerages and plans to roll out the system in New Zealand.

Steadfast shares in efficiency gains through equity brokers, as well as through increased management and administration fees. As a result, we see Steadfast’s earnings growth accelerating as its IT costs moderate and its revenues grow.

Conclusion

IML continues to steer away from the highly valued, high risk and in our opinion often dubious quality of the majority of technology stocks listed on the ASX. Instead we prefer to invest in well-established industrial companies that are looking at making their activities more efficient through the use of technological innovations which we believe will ultimately improve the quality, efficiency and reach of their existing business models. This fusion of new technology and well-established businesses will underpin the earnings growth outlook for many of IML’s existing holdings in the next 3 to 5 years.

While the information contained in this article has been prepared with all reasonable care, Investors Mutual Limited (AFSL 229988) accepts no responsibility or liability for any errors, omissions or misstatements however caused. This information is not personal advice. This advice is general in nature and has been prepared without taking account of your objectives, financial situation or needs. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to buy, sell or hold that stock.

INVESTMENT INSIGHTS & PERFORMANCE UPDATES

Subscribe to receive IML’s regular performance updates, invitations to webinars as well as regular insights from IML’s investment team, featured in the Natixis Investment Managers Expert Collective newsletter.

IML marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected by Natixis Investment Managers Australia, on behalf of IML. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.